My father is by education an electrical engineer, and by vocation an early implementer of computers into the telephone company. While I gained enormously from the things he shared with me in those fields, what has probably helped my most in life is his financial advice to us kids. I’ll will share some of these here.

Yuko’s mother lives with us. She can still get around the house herself but suffers from dementia, sometimes a lot worse than other times.

She is no longer able to work the TV and AC remotes, etc. (See some of my other posts for the workaround we did for this.)

A couple of months ago, she got up in the night to use the bathroom, and couldn’t find her way back to her bedroom, so was wandering in the hall till Yuko realized something was wrong, and went downstairs and helped her back to her room.

This happened two nights in a row. I tried to think of some way to help, and remembered the “emergency lighting on the floor” that they always talk about on airplanes before takeoff.

You can buy similar products online, so I bought a string and drew a path from her bedroom door to the bathroom. We leave them on night and day. She has not lost her way since.

Another simple one for care givers out there. Yuko’s mom has to take medicine but can’t see very well.

The more she can do on her own though, the better she feels and the better off we all are. We used to place a couple of tablets in her hand so she could take them, but by the time they got to her mouth usually one had rolled off her hand and fallen to the floor.

We finally solved this by putting a small dish on the table. She can see the dish and feel around to pick up the tablets, which she will always do one at a time with her thumb and forefinger, which means they make it to her mouth.

Working from home means even less exercise than I was getting when I was in Tokyo. At least there I had the walk with the commute.

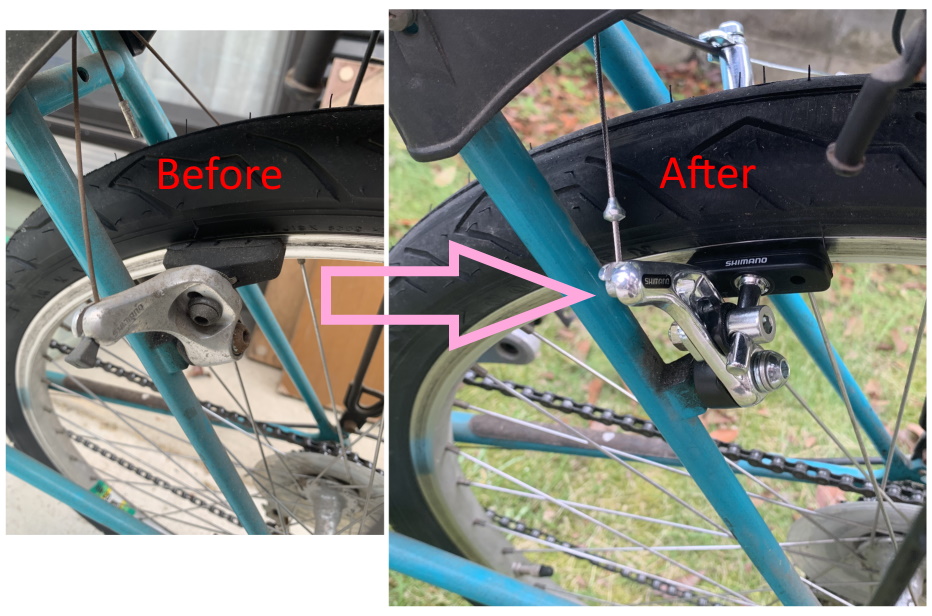

So, I decided I needed to do at least some sort of exercise. For me, riding a bicycle is about the only exercise that I actually enjoy. Of course, my really nice bike that I bought is stuck in my apartment in Tokyo, so I pulled out my Miyata out of the plastic shed around the back of the house.

I hadn’t ridden it in a while, but I have the urge every once in a while so it wasn’t in totally bad shape. The years have in fact taken a bit of a toll though. I could tell the brake shoes had hardened up, so I figured I would just order some new brake shoes. Sorry, Shimano doesn’t make these any more. They have a period of 7 years that they keep parts for stuff they don’t make anymore, but I must have bought this bike in 1991 or 92 or so. (It even says “made in Japan”!)

So, after several failed attempts to make other brake pads work, and after a LOT of research, I found a set of Shimano cantilever brakes (the entire assembly, both front and rear) that I hoped I could make work.

Never having done this before, it took some doing, but I in fact got them installed and they seem to be working. In case anyone is interested, the “new” brakes I got are Shimano model BR-CT91.

Also, note that while Shimano sells a FRONT and REAR part for these, I checked around and everyone was saying that the hardware is exactly the same–only the brake shoes are swapped. Since the REAR part was out of stock, I got two FRONT assemblies and swapped out the shoes left for right, and can’t see any issues. (Honestly on this model, even the shoes appear to be interchangeable.)

I think Junior High School (secondary school) age is where kids really change their perspective on life as they know it–whether from their own hormone changes or society or whatever. In any case, my Dad knew that the same kinds of simple lessons he had been teaching us younger kids were not going to cut it when we hit Junior High.

By this time we knew all the basics–how to save and how to work, how to earn, etc. Now my Dad wanted us to get a taste of…hmmmm, maybe it was financial failure.

No longer were we to receive an “allowance” like we had done in the past, which was discretionary money over an above what our parents spent on us for room, board, clothing, etc. No, Dad had another idea. He had us kids create a BUDGET.

Now, once again Dad made this at least approachable for us kids. All of our food and board was just paid for as part of being in the family. But he knew that CLOTHING was now not just a necessity, it was a WANT. In other words, I wasn’t going to be happy with a pair of sneakers for basketball, I was going to want a specific brand of white leather sneakers that were EXACTLY WHAT EVERYONE ELSE WAS WEARING and probably cost twice as much as what the “just functional” pair of sneakers cost.

He knew that we were going to get into sports or other clubs that cost rather significant amounts of money. We were going to be involved in church and other activities (later dating) that cost money. We were going to want to buy records, stop on the way home for ice cream to socialize with our friends, etc.

He also knew we needed to learn about CASH FLOW.

Therefore, all of a sudden our allowance stopped. Instead, we had to create a YEARLY budget, and get it approved by the Minister of the Department of the Interior (Mom), and then submit it to the head of the Treasury Department (Dad) for dispersal.

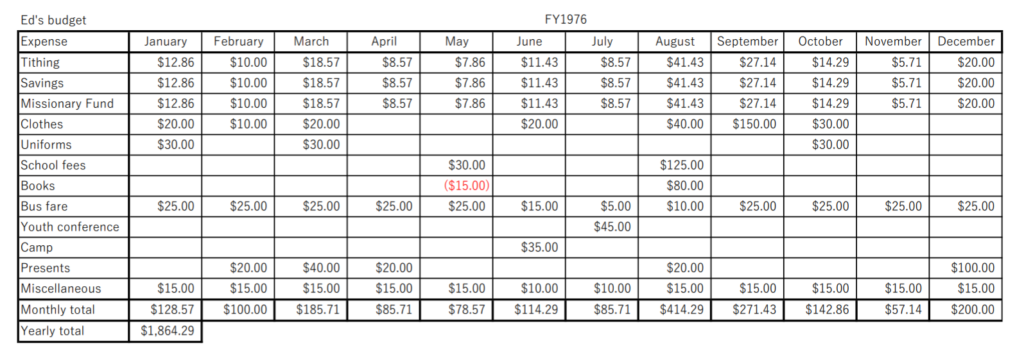

What did this mean? We had to make list of all the expenses we were going to have, and in which month out of the year they were going to occur. Our fiscal year started in January (important because back-to-school was generally the most expensive month, and did not happen till August/September). On this list were things like clothes, haircuts, fees for clubs including gear, fees for events (Youth Conference, camps, etc.), Christmas and birthday present expenses, school supplies and fees, bus fare and later gasoline expenses, that wonderful “miscellaneous expense” and of course, Tithing, Savings, Missionary Fund–which of course had to be back-figured since it would be 10% of what we would be getting. At least, I first assumed that I would be getting the needed amount on a month-to-month bases.

A sample of what my budget would have looked like. (If I had Excel back then, which of course I did not, so it was the above only hand-written.)

Basically, everything that was an out-of-pocket expense had to be on the list. Mom was no longer doing clothes shopping for me. I wanted to be as independent from her as possible. I wanted to pay all my school and church stuff without her hanging around.

I remember slaving over this list. Trying to guess all the different things I might have to spend money on. Once I got the list done, then I had to realize that this was 70% of the money I was going to ask for, because I also needed to get the 30% for Tithing, Savings, and Missionary Fund. I started to see how math actually helps in “real” life.

Then, I would take the list to Mom. At this point we would discuss discuss both what I had on the list (exactly what was included in “miscellaneous expenses” what usually the hardest part), and whether the amounts were appropriate or not. She was strict, but actually very helpful, and reminded me of things I forgot to include. It usually took a couple of rounds to get it to the point of being ready to submit to the Treasury Department.

When it got to Dad, he would usually whistle and say something like “that’s a lot of money for someone your age”. The effect of this was to scare me to death but at the same time make me feel very responsible.

Now, remember that I have made a budget for a year on a MONTHLY basis. August/September always had a huge amount of money because of needing new clothes, having to pay for school expenses and club fees, etc. December was another big one because of Christmas presents. But what did the head of the Department of Treasury do? He said, OK, your total budget for the year is X, and I will pay you in EVEN MONTHLY PAYMENTS of X/12.

He was nice enough to then walk me though my “cash flow” plan. “See how August is going to eat up 3 months worth of your monthly stipend? You better have that much in the bank when you get to that point in the year or you will be wearing last year’s fashion that will also be too small for you!”

What a very simplified cash flow view might have looked like if we had Excel back then.

That fear kept me saving. But if something came up I might sneak a little beforehand. “I can get by with 3 shirts instead of 5” I would tell myself. Yeah, well it didn’t always work out that way. To be honest, the first year I was on the budget plan we did have to have an emergency meeting of congress (the family) to determine if relief could be provided for “over-budget expenses not previously approved”. The younger kids were amazed but also scared to death at the amount of money in my budget, and knew that their turn was coming, so they dare not say anything to derail approval of additional budget allowance.

Although very painful for the first couple of years, by high school I was pretty proficient at forecasting and calculating, as well as pleading my case for those “miscellaneous expenses”.

But now that I have become an adult and have opportunity to talk with others who never had the chance of experiencing these kinds of things in a safety net environment, but instead entered society without first learning them, I realize that this stuff is not self-evident to people.

I have been approached by people who say “if you can just loan me 50,000 yen (about $450 USD) I will be fine”. Being the stickler that I am I make them do a three-month budget and can usually show them that because of cash flow issues the 50,000 yen would only keep them going for a couple of weeks, and they really need 200,000 yen, and that if they don’t either cut expenses or increase their income, even that won’t work in the long term.

Honestly, I hate all things that have to do with finance. I hate doing budgets. I don’t think I have ever done as detailed a budget since I have been in the workforce as I did each year when I was a student and was still living off my parents. I have been blessed to always have a good-paying job (of course I have taken cuts when the company has done poorly and gotten bonuses when it did well), and a pragmatic wife who has handled our money since we were married. But I think my father’s teaching allowed me to develop an ability to know if I am getting into trouble before it happens, and spurs me to immediately take steps to mitigate the trouble. I know how to do budgets and can immediately teach anyone else how to do one, and how to check their cash flow using a notebook from the 100 yen shop.

Another thing my father taught us besides instilling in us the idea of Tithing, Savings, and Missionary Fund, was to work and save to get something we wanted. He did this by a “matching” scheme.

Actually, once we were old enough to understand, my Dad would tell us that whatever amount we had saved up for a Mission by the time we were 18, he would “match” that amount. But, he also applied that to some other things that were “big” to us at each stage of our lives.

So, for example, when I was in second or third grade, I saw this 10-speed Stingray bicycle at the store one time and really wanted it. It cost about $70. Based on the amount I was getting as an allowance at the time, even if I saved everything I probably would have outgrown the bike before I would have saved enough to buy it. It seemed totally out of reach. I was hoping maybe Dad would give it to me for a birthday or Christmas present–even though I knew it was a bit too pricey for such. So, after my Dad talked with me long enough to test my resolve, he agreed that the bike could be a “match it” purchase.

What that meant is that somehow I had to get $35 dollars together, and he would chip in the other $35 dollars. As I remember I already had $5 -$10 to start. I then proceeded to go to neighbors and offer my services to mow their lawn or weed, etc. for a fee. Some accepted. Allowance day was always big — the whole thing went into my bike savings — I wasn’t going to spend it on candy or trading cards or anything like that. And because Dad was willing to pay me for washing and vacuuming our car, it was spotless for several months. I seem to remember that it took me about 4 or 5 months to get to the $35 dollars. Every couple of weeks I would go to the store and make sure the bike was still there. And by the time I was down to earning the last $3 dollars I had pretty much tapped everybody out. I was going to get a loan from my siblings when they got their allowance but Dad stopped that. (“Loans are for homes, not bikes.”) I am pretty sure Dad let me clean an already clean car to help me over the top.

But sure enough, I made it. And I enjoyed that bike and I took care of it like you wouldn’t believe-keeping it out of the weather at night and even learning how to do maintenance on it.

For 35 bucks, my father taught me: 1. The value of work, 2. The value of money, 3. To EARN what I receive, 4. I can ACHIEVE what I set my mind to.

When I think about it, I am sure Dad realized that I never would have been able to save the full price for that bike, so he knew I would have lost interest as it would have been hopeless. On the other hand, he knew that I could do half if I really tried. He then made sure I would succeed if I really tried. (Remember those payments for washing an already-clean car?)

Later in life, this served me well. Can I afford to get a used car right now? Can I afford to buy a computer? Can I afford a trip to…?

Nowadays, we as a society are so prosperous that our kids pretty much get anything they want IMMEDIATELY when they want it. (Do your kids have the latest Nitendo or other “game”? Did THEY buy either the player or the games?) As parents we will probably have to create ways to teach these important concepts to our children because if we go with the flow we will create in our children a feeling of “entitlement” that is more like “the world owes me things”.

Besides instilling in us the idea of Tithing, Savings, and Missionary Fund, as we moved into later elementary school years, my Dad used a method to teach us about how to take responsibility for our financial outcomes.

The first way was to teach us that we were part of a family which included the finances to run the family, and not just independent beings. I am sure this lesson took a bit of preparation on his part. Here is how it went.

He would bring out a bunch of money from our Monopoly Game. He would then line up what looked like a bunch of money to us kids, and say, “This is how much money I make in a year.”

Wow, to us kids, this looked like a HUGE amount of money. Then he would begin paying our “bills”, starting with Tithing, Savings, and Next Big Life event (that was my parent’s mission), but would of course move on to house payments, utilities, food, clothes, and even get closer to us with school fees, PTA money, etc. At the end there would be just enough money left to pay us kids our “allowance”, and all the money would be GONE.

Then he would say, “Dad works to make this money to support the family, because he is the Dad and because that is his role in the family. Mom works hard in the home and takes care of all kinds of stuff because she is the Mom, and because that is her role in the family. You kids study hard, and help around the house and do your chores because that is your role in the family. You get allowance because the family has enough money to give it to you. It is NOT payment for doing your chores.”

Now, don’t get me wrong. Dad made up all kinds of jobs around the house that we could do to be paid for. But cleaning our own rooms, and doing the tasks that we were normally assigned to (like emptying the garbage, mowing the lawn, etc.) were not part of these. (I remember washing the car being one of the “for pay” jobs.)

This was really interesting to me, because it showed me what “entitlement” is really supposed to mean–that I am entitled because I am part of a group (the family) with responsibilities for each member: that when all work together will generate something that can be shared-and we are entitled to our “share” once it is generated.

When us kids were very young, as in lower grades of elementary school, my father would do the usual “1 of ten coins is for tithing” lesson, but with a bit of a twist. He would show us a dollar. Then he would show us a bunch of dimes (10 cents) and have us kids create the equivalent of the dollar. Then he would say “What should you do when you earn a dollar?” All of us kids would dutifully answer with what we learned at church that we should first take one dime and pay our tithing. But Dad didn’t stop there. He proceeded to tell us that we needed to “save for a rainy day” and we also needed to “save for our next big life event” (which for us kids would be a mission). So, he had us all make three “banks” -one for Tithing, one for Savings, and one for Missionary Fund. These were jars that we labeled, and cut a slot in the lid to put the coins in. However for the Savings and Missionary Fund jars, we also taped the lids shut. Of course the point was that we would not be tempted to take out the money early-these were long-term savings. And if my father ever gave us money (for an allowance or even as a birthday present), he always made sure that it was already in a form that it could be distributed between those three jars.

Later, when the jars got so full that no more would fit, we would have kind of a big ceremony where we would open the jars and count how much money was in there, and Dad would give us paper money to replace the coins so that we would have more room. And when we got a bit older, instead of doing that he would take us down to the local bank and open a savings account there-starting with the bottle of money that our Savings had.

I am not very adept at soldering, so in general I don’t do repairs of electronics at the board level. But the idea of having to pay Apple quite a bit of money to replace an ailing battery just rubbed me the wrong way. I had an iPhone 6 plus. The battery was not holding a charge very long. This particular phone was actually part of the giant “we’ll replace it for USD $29” scandal, so it wouldn’t have set me back that much, but since I was considering getting a new phone anyway, I decided to try to replace the battery on my own just to see if I could get comfortable doing such a thing.

The first “go to” place on do-it-yourself gadget repair is ifixit. They have all kinds of guides, and will sell kits as well. I basically followed their guide to replace the battery in my iPhone 6 plus, and old iPhone 4, and an iPad mini 2. Each of the guides are reasonably good, but here is what I would do differently, or what I now feel is common sense.

You can probably get the replacement batteries on Amazon or Aliexpress. The quality of all these batteries is all questionable in my mind. I at least try and find ones with the PSE mark (which of course could also be fake). I look at comments and try and see if most are fake comments or real. Also, it seems these batteries have a warehouse shelf life. Some companies will advertise a “less than six months old” policy that may be worth it. (I had one iPhone 4 battery that was DOA.)

Don’t do this when you are in a hurry. They have a reference time on some of the guides. Just assume you are going to need a couple of hours.

Take the time to cover your work area with light-colored paper or a plain table cloth. You will almost always lose a screw or other little part, and usually you will want to find it.

Print out the guide unless you have an extra tablet to view. Mobile phone screens are too hard to focus on when you are back and forth with your work.

I like to print out a photo (your own or from ifixit) on A4 (or Letter-size) paper and then put double stick tape next to each screw in the photo. Then, when I take out a screw, I set it on the double stick take next to its own photo, and that helps me get the right parts back in later.

You can make the heating pad that is shown on ifixit out of socks and rice. I found that men’s socks are too big as socks will stretch quite a bit as they are filled with rice. Also, sewing through (like a quilt) in a few places helps keep the rice a bit more evenly distributed. When you heat this in the microwave, a fair amount of moisture will come out. Use common sense when putting it on the device. I found that setting the device in front of my kerosene fan heater got things pretty warm, and then I put the socks/rice heating pad on that for the final touches.

I would suggest you buy a new set of screws for the device before you start. Aliexpress has these for very little money–just get a set.

Ditto with the “seal sets”. Aliexpress will have them. These are some sort of seal adhesive that is set in the same shape as the screen. When you remove the screen, you essentially heat this stuff up so that the screen will come off. The seal is typically somewhat damaged in the process. The phone will still go back together just fine, but my guess is the water-resistance is significantly decreased.

If you assign a value to your time, then I would say it is NOT worth it to replace iDevice batteries yourself. However, if you look at the time you spend fixing it as recreation, then you can save a significant amount of money doing it yourself.

My mother-in-law unfortunately has dementia to the point that she has forgotten how to use a television remote. She watches television, but pretty much only NHK (Japan’s national channel) and the all-the-time-samurai-movie channel. Everytime she got sick of one of these, she would come in and ask us to change the channel to the other station. Either my wife or I would have to get up and go into her room to change the channel for her–not a big deal-but a bit inconvenient nonetheless.

Since I had already used a “Black bean” to deal with the air conditioner at my apartment, I knew there was an easier way to do this. I looked around a bit more and found a product similar to the Black bean called the Orvibo Magic Cube.

I chose this product because it seems to have better support for Amazon Alexa/Google Home/Siri, and I was thinking if somehow I could hack one of those machines so the my mother-in-law could just say “NHK” and have the channel change, that would be cool. I haven’t got that far, but in the companion app to the Orvibo Magic Cube, I have two macro buttons. One is for the NHK channel, and the other is for the Samurai Movie channel. Now when she comes in, I just ask which channel she wants, and the deed is done!